Ever since I was on the client side of the wealth management industry, the Great Wealth Transfer has been a core narrative from tech vendors: billions of dollars are changing hands, 70% to 90% of heirs will fire their parents’ advisor, and the only way to stop it is to buy a sleeker digital portal.

It’s a great pitch for selling software. And it’s not entirely wrong—digital maturity does matter, particularly to Millennials and younger generations. But from what I’ve seen in the data, it isn’t their primary driver when selecting an advisor.

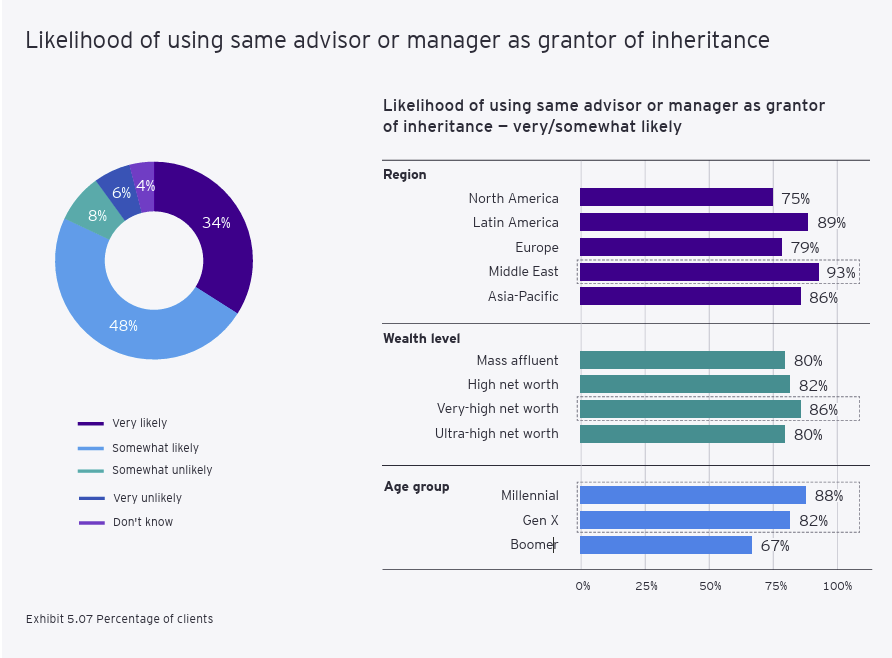

The 2025 EY Global Wealth Research Report surveyed 3,600 wealthy clients worldwide and found that 75% of North American inheritors say they’re likely to continue with their benefactor’s advisor. That sounds like a retention story—but “likely” includes “somewhat likely,” which is a soft commitment at best. And 25% are already saying they’ll probably leave—before any friction even enters the picture.

The generational split is where it gets interesting. 88% of Millennials say they’re likely to stay, compared to 67% of Boomers. Younger inheritors claim more loyalty—but as we’ll see, their behavior tells a different story.

Source: EY 2025 Global Wealth Research Report, Exhibit 5.07

So if most inheritors say they’ll stay, why do so many end up leaving? And what role—if any—does digital maturity actually play?

The Biggest Risk Isn’t Your Technology

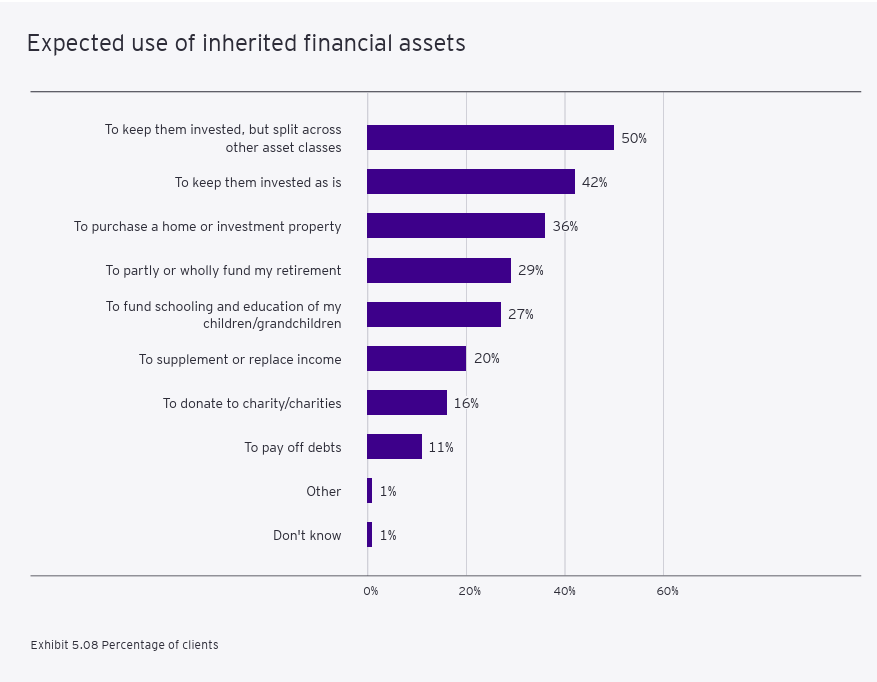

Look at what inheritors actually plan to do with the money the moment it transfers. According to the same EY study:

-

50% plan to keep assets invested but split them across new asset classes.

-

42% plan to keep them invested as is.

-

36% will liquidate to purchase real estate or investment property.

-

29% will redirect the capital to fund retirement.

Source: EY 2025 Global Wealth Research Report, Exhibit 5.08

Even the 42% who plan to keep assets invested as is aren’t guaranteed to keep the same advisor—they’re expressing an investment preference, not advisor loyalty. And the majority of inheritors are planning to do something different with the money: reallocate, restructure, or spend.

If your business model is designed entirely around wealth preservation—and, in my experience, most traditional wealth managers’ models are—you have limited relevance to an inheritor whose financial objectives look nothing like their parents’.

A portal isn’t going to bridge that gap. And no app, however elegant, creates a relationship where one doesn’t exist. Capital flight during wealth transfer isn’t primarily driven by clunky login screens—it’s driven by a misalignment between what the advisor is focused on and what the heir actually needs.

If you haven’t done it already, the research suggests that adapting your business model to the core needs of your future clients is the most important step to ensure you retain assets.

It seems obvious, but as many of us know, it’s sometimes the obvious that’s the easiest to miss.

But that doesn’t mean digital maturity is a nice-to-have sitting beside the real work. It’s a key part of the infrastructure—the vehicle—that makes the real work possible.

Where Digital Maturity Actually Moves the Needle

To be clear: while a polished portal isn’t going to save a relationship that’s fundamentally misaligned, digital friction will absolutely hinder client acquisition or accelerate an heir’s exit.

When I worked at Gluskin Sheff—a Toronto-based boutique wealth management firm for high-net-worth investors, since acquired by Onex and then RBC—I once helped a wealthy prospect resolve a small technical issue accessing our economic research. It was a brief interaction—nothing I thought twice about at the time. But I later learned it had left an impression on the prospect. When the advisor thanked me for looking after his client, he put it simply: every bit matters.

“Every bit matters.”

That line stuck with me, and I’ve thought about it often since. Every interaction a prospect or client has with your brand—whether delivered by a person or a platform—shapes their perception of the firm. In an environment as competitive as wealth management, I’ve come to believe there are no neutral touchpoints.

What makes this especially urgent is that the bar isn’t being set by other wealth managers. It’s being set by every other digital experience your clients have. Alpha FMC’s 2024 research on digital experience in private wealth found that investor expectations aren’t formed within the wealth management industry—they’re shaped by how clients interact with digital services across their entire lives.

J.D. Power’s 2025 Wealth Management Digital Experience Study echoes this: the growth of fintech players has raised the bar on what investors expect from a personalized digital experience. Your clients compare you to every app, platform, and service they use—not just to the advisor down the street. Plus, in my experience, it’s not uncommon for these wealthy heirs to have a Wealthsimple or robo advisor account before they inherit their fortunes, which means that digital maturity is their baseline.

Investor expectations aren’t formed within the wealth management industry—they’re shaped by how clients interact with digital services across their entire lives.

The data bears this out.

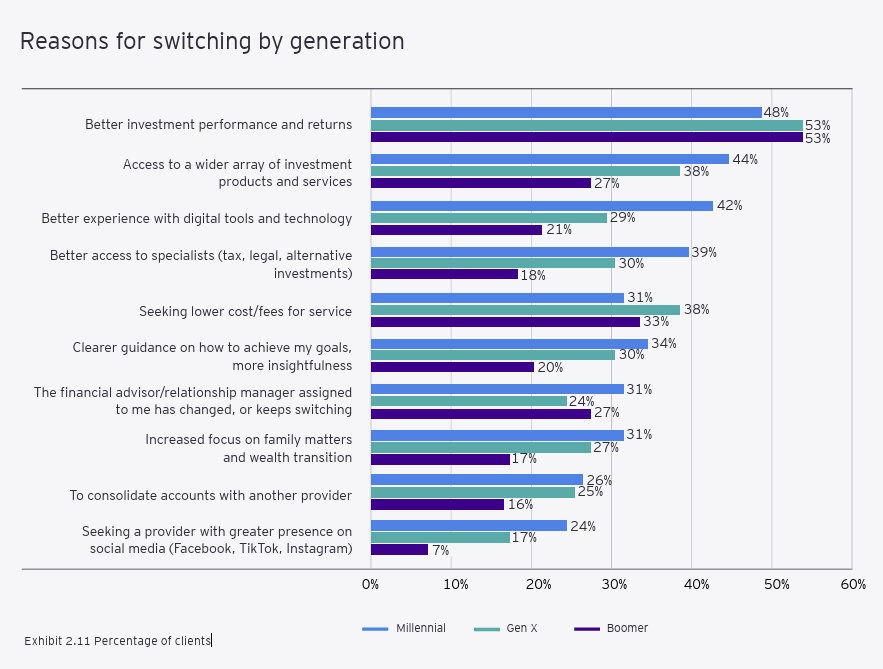

Millennials are already leaving for better digital. Remember that 88% of Millennials who say they’re “likely” to stay with their inherited advisor? That same EY study found that 42% of Millennials cite the need for better digital tools as a primary driver for switching—making it their #3 reason for leaving, compared to just #5 for Boomers. They say they’ll stay, but their switching triggers suggest otherwise.

They say they’ll stay, but their switching triggers suggest otherwise.

The moment of transition—when loyalty is already soft—is exactly when those instincts are most likely to activate.

Source: EY 2025 Global Wealth Research Report, Exhibit 2.11

Heirs are starting their search on Google and AI. 25% of affluent Americans are now using AI tools to begin their search for a new financial advisor. Think about that for a moment. If your firm doesn’t show up when an heir searches online or asks an AI assistant about wealth managers who specialize in their situation, you’re not even in the consideration set. And for firms that do show up, your digital presence is the first impression you make—and possibly the last.

Source: Wealthtender, “How Americans Will Choose Financial Advisors in 2026 and Beyond,” 2025 (n=500)

Our own competitive research validates this. A recent Semrush analysis we conducted of CIBC Global Asset Management’s web traffic found that 52% of their visits now come from AI-powered sources—including LLMs and Google’s AI Mode. Over half. Where do you think that number will be in two years? Doing the work to ensure your firm shows up in AI-generated results is no longer optional.

Better digital experience drives retention and trust. J.D. Power’s 2024 U.S. Wealth Management Digital Experience Study found that investors whose digital experience meets “foundational and findable” quality levels report satisfaction scores roughly 100 points higher on a 1,000-point scale. That’s not a rounding error. Alpha FMC’s research found something similar: each 10% increase in digital satisfaction corresponds to a 15% higher likelihood of a client becoming a net promoter of their wealth manager. For firms navigating the wealth transfer, that link between digital quality and advocacy matters—because the next generation is forming impressions of your firm right now, whether they’ve inherited the relationship yet or not.

Sources: J.D. Power, 2024 Study; Alpha FMC, 2024 CX Benchmark

Digital maturity gives advisors time back for relationships. This is the one that, for me, ties the whole argument together. McKinsey estimates that AI and digital maturity could free up 20 to 30 percent of advisor time currently spent on administrative tasks. That’s not a technology talking point. That’s the capacity your advisors need to do what actually prevents capital flight: building multi-generational relationships before the transfer happens.

Source: McKinsey, “US Wealth Management in 2035: A Transformative Decade Begins,” January 2026

The Real Opportunity

Vendors have overstated—and in many cases misrepresented—the impact of digital maturity in preparing for the Great Wealth Transfer. But they aren’t entirely wrong. The impact is real.

Digital maturity doesn’t prevent capital flight by making your client portal prettier. It prevents capital flight because digital expectations have risen, every bit matters, and understanding what each heir actually needs is much easier when they’re not already frustrated by the experience of interacting with your brand.

The retention lever isn’t technology for technology’s sake. It’s technology that frees advisors to deliver the depth of service that actually keeps assets in place—and that shows up credibly when the next generation starts researching who should manage the wealth they’re about to inherit.

Firms that understand this distinction—that prioritize investing in digital infrastructure so they can meet prospects and clients where they are—give themselves a better shot at retaining the next generation of wealth.

McKinsey, “US Wealth Management in 2035: A Transformative Decade Begins,” January 2026.